Do You Qualify for Spousal Social Security Benefits? 3 Things to Know Before Applying

Millions of Americans rely on Social Security retirement benefits to provide a financial safety net in their golden years, making it one of the country's most important social programs. It's also a well-earned reward after years of paying Social Security taxes from virtually every paycheck.

Although Social Security retirement benefits are based on people's work history, not everyone has worked or earned enough to receive a substantial benefit. Luckily, Social Security retirement benefits aren't solely for those who have worked and paid taxes through the years. Social Security allows spousal benefits to support non-working or low-earning spouses in retirement.

For any couple nearing retirement and considering this as an option, here are three things you should know about Social Security spousal benefits.

1. Who is eligible to receive Social Security spousal benefits

To qualify for Social Security spousal benefits, you must be married for a year, your spouse must currently receive retirement benefits, and one of the following must apply:

- You're at least 62 years old.

- You're caring for a child under 16.

- You're caring for a child with a disability.

If you're at least 62 and your spouse hasn't claimed benefits yet, you can claim your own benefits and then claim their higher benefit once they begin receiving them. This is a good option for couples with an age difference or a situation where the primary claiming spouse wants to delay benefits longer for the increased monthly payout.

If you're currently divorced, you may be able to claim spousal benefits based on your former spouse's work history as long as you were married for at least 10 years.

2. How your claiming age affects your monthly benefit

For the spouse claiming standard benefits, Social Security calculates your monthly benefit amount using a formula that takes into account the 35 years when your earnings were the highest. It adjusts the earnings for inflation to reflect their value in today's dollars and then divides them by the number of months in those 35 years. If you don't have 35 years' worth of income, Social Security uses zeros for the missing years to calculate your average.

From there, Social Security will determine the amount of the benefit for the person claiming spousal benefits. Assuming the person claiming spousal benefits is at full retirement age (FRA), they can receive 50% of their spouse's primary insurance amount. For example, if spouse A's earnings record gives them a monthly benefit of $1,500 at their FRA, spouse B could receive up to $750 monthly.

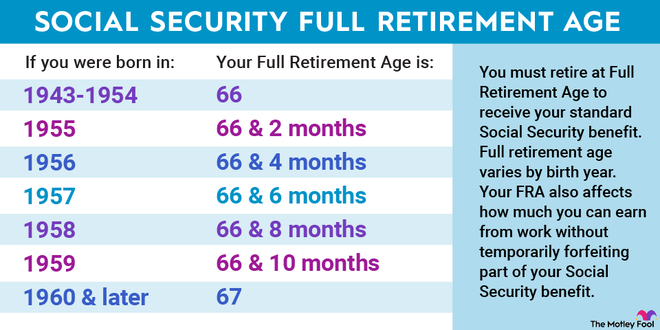

FRAs are based on birth years as follows:

Like standard benefits, you can claim spousal benefits before your FRA, beginning at age 62. For the primary claimer, benefits are reduced by 5/9 of 1% each month before their FRA, up to 36 months. Each month after that further reduces benefits by 5/12 of 1%.

COLA:2025 Social Security COLA estimate slips, keeping seniors under pressure

For those receiving spousal benefits, benefits are reduced by 25/36 of 1% each month before their FRA, up to 36 months. After that, benefits are reduced by 5/12 of 1% monthly. For instance, if your FRA is 67 and you claim spousal benefits at 62, your monthly check will be reduced by 35%. If you claim at 64%, it will be reduced by 25%.

Unlike standard benefits, spousal benefits aren't increased if you delay claiming past your FRA.

3. Social Security spousal and survivors benefits are closely linked

If you're claiming spousal benefits when your partner passes away, Social Security will automatically convert your spousal benefits to survivors benefits. Survivors benefits make you eligible to receive up to 100% of your deceased spouse's benefit, including any benefit increase they may have received from delaying benefits.

A widow or widower can begin receiving survivors benefits at age 60, or 50 if they're dealing with a disability. However, like standard and spousal benefits, the monthly payout will be reduced if claimed before FRA.

You can't simultaneously receive spousal and survivors benefits, only the higher amount. Since spousal benefits max out at 50% of the partner's primary insurance amount, survivors benefits are generally the higher-paying option.

This close link between Social Security spousal and survivors benefits is important because it provides critical financial assistance after a partner has passed away.

The Motley Fool has a disclosure policy.

The Motley Fool is a USA TODAY content partner offering financial news, analysis and commentary designed to help people take control of their financial lives. Its content is produced independently of USA TODAY.

The $22,924 Social Security bonus most retirees completely overlook

Offer from the Motley Fool: If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. Simply click here to discover how to learn more about these strategies.

View the "Social Security secrets" ›

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.