How to turn modest retirement contributions into a small fortune over time

Do you feel like you can't tuck enough money away for retirement right now to actually matter in the future? You're not alone. Plenty of people feel this way. It's a particularly common assumption among young adults who are not yet in their prime-earning years and who have seen life's costs outpace wage growth most of their lives.

Don't fall into the pessimism trap! The conditions prompting the assumption are deceptive. You can beat inflation, even with the smallest amounts of money being chipped into your retirement nest egg. The key is time. It takes a lot of it before the earnings on your past investment gains start to make more of a positive difference than your annual contributions to a retirement account do.

Never too young to save for retirement:Why a custodial Roth IRA may make sense

The power of compounding

It's called compounding. In simplest terms, it just means reinvesting your dividends, interest, and gains on previously saved money in order to accelerate the growth of these dividends and gains in the future. Compounding can help turn even modest amounts of money into a small – or even large – fortune.

The catch? You have to wait a while to start seeing serious growth from compounding take meaningful effect.

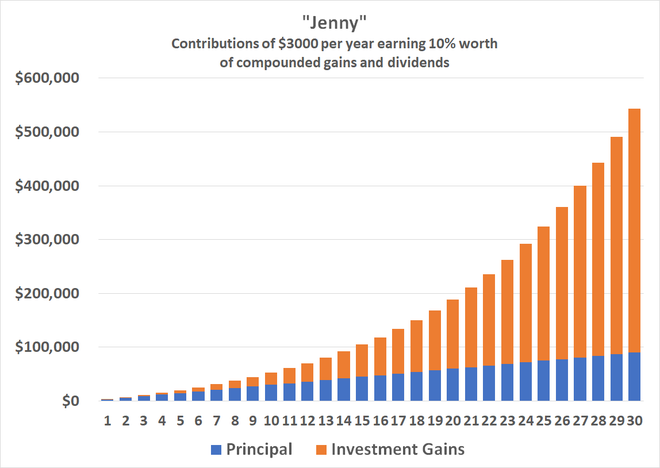

An example will help illustrate the idea. So, let's use a hypothetical 30-year-old named Jenny to make the point.

Jenny owns a small landscaping business. After paying her employees and covering her expenses she clears about $60,000 per year. Living in the suburbs of a major metropolitan area, though, her living expenses use up most of that money. She can only scrape together an extra $3,000 every year to put toward retirement. Jenny fears that's not enough to even make it worth her while, so she just spends it on other things instead.

That's a mistake. Although $3,000 might not feel like a life-changing amount of money right now, saving that extra $3,000 every year over the length of a career is a big deal. After 30 years of work, that's $90,000.

But that's not the most exciting possibility of committing to saving even modest amounts of money as you earn it. If she were to put that $3,000 into an S&P 500 index fund every year and earn the broad market's average annual return of 10% – and reinvest any dividends collected along the way – Jenny would end a 30-year stretch with over $500,000.

Can't come up with $3,000 per year? That's OK. It's possible to do even more with less -- if you have more time.

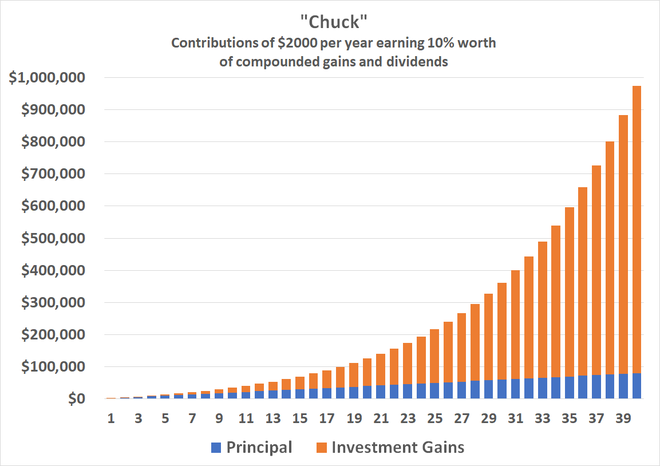

Let's work through another example. This time, it's Chuck, a 25-year-old construction worker earning $40,000 per year. He plans to work until he's 65. Chuck knows he'll be earning more in the future as he gains experience, but he also knows he wants to have a lot of children, so there may not be much more than $2,000 per year to contribute to retirement savings.

He's not risk-averse, though, and is willing to put that money to work in the stock market where he'll be achieving the same kinds of returns Jenny will. How much will Chuck be sitting on at the end of his 40-year career? An incredible $973,000.

Impressed? You should be. A mere $80,000 worth of savings accumulated over four decades can turn into nearly $1 million by the end of that period. Of course, it was time that did the bulk of the heavy lifting.

If you're a millennial who's been too discouraged to even start putting your money to work in a retirement fund, this is an encouraging eye-opener to be sure.

Just stay the course

There are a couple of warnings to add. First, although the hypothetical portfolios above grew in a straight line, yours won't.

While the S&P 500's average annual gain is around 10%, that historical performance is not guaranteed going forward. And even if the market does follow a similar trajectory over a 30- or 40-year stretch, you won't achieve that exact gain every single year. Some years you'll do worse; other years you'll do better. You'll even lose ground in some years, but don't sweat it. Investing for retirement is a marathon rather than a sprint.

And the second warning? Note than neither Chuck nor Jenny started seeing yearly investment gains that were bigger than their annual contributions to their retirement fund until they were about two-thirds into their savings period. It was pretty slow slogging until then, with seemingly little progress being made. It was only in the last one-third of their savings period that compounding finally appeared to drive explosive growth (although once it did, wow!).

Don't be fooled by this apparent dynamic, though. To get to the last leg of your savings and investing years where the big gains happen, you have to keep pushing through that slow initial period of your saving years when it seems like you're not making much progress. Despite how things look, you're setting up an important foundation.

Still don't know where or even how to start? Start here.

James Brumley has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The Motley Fool is a USA TODAY content partner offering financial news, analysis and commentary designed to help people take control of their financial lives. Its content is produced independently of USA TODAY.

10 stocks we like better than Walmart

Offer from the Motley Fool: When our analyst team has an investing tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now... and Walmart wasn't one of them! That's right – they think these 10 stocks are even better buys.

See the 10 stocks

*Stock Advisor returns as of MM/DD/YYYY

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.